India’s Cotton Exports Drop By 55% Amid High Domestic Prices

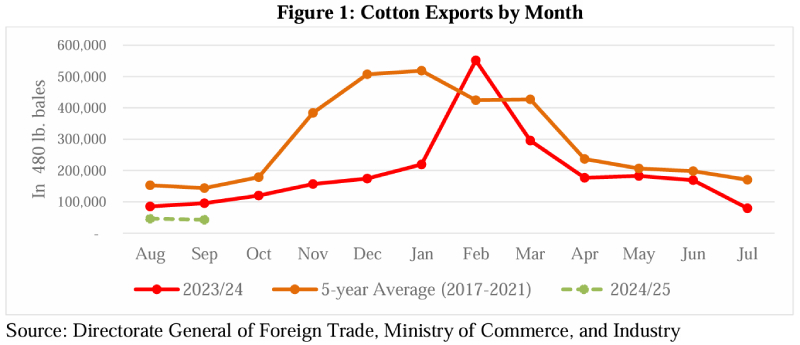

India’s raw cotton exports are projected to decline significantly in MY 2024/25, falling by 55% to 1.2 million 480-lb bales, according to FAS Mumbai’s October 2024 report. Domestic lint prices, trading 4% higher than global rates, have made Indian cotton less competitive internationally. Buyers are increasingly opting for finer-quality, machine-picked cotton from other sources. Improved domestic mill demand has also reduced the exportable surplus as more raw cotton is allocated for value-added products.

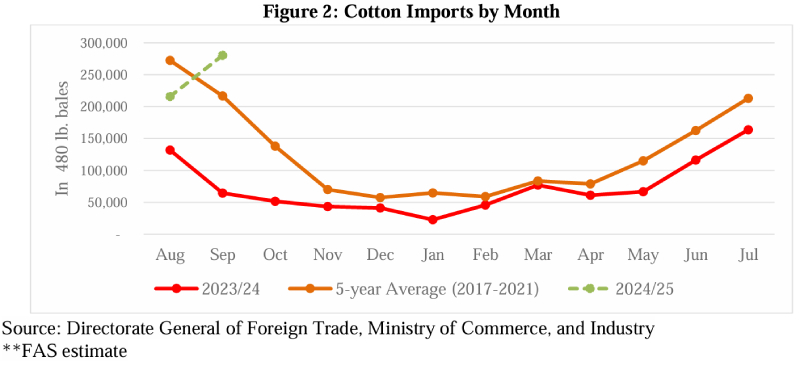

The forecast for Indian cotton imports in MY 2024/25 has risen by 67%, reaching 2 million 480-lb bales. Mills are importing higher volumes of premium-quality cotton to fulfill export commitments for high-value textiles. September 2024 data reveals a 240% year-on-year increase in raw cotton shipments, dominated by supplies from Australia (38%), the United States, and Mali (16% each).

India’s cotton acreage for MY 2024/25 is estimated at 11.8 million hectares, a 9% decrease from the previous year, as farmers shift to higher-return crops like paddy and pulses. Unseasonal rains in southern India further affected planting patterns, leading to replanting in some regions. Despite the reduced acreage, production is forecast to remain stable at 25 million 480-lb bales, aided by improved yields in southern India.

India’s domestic mill consumption is forecast at 25.5 million 480-lb bales, driven by steady demand from the textiles and apparel sectors. Cotton yarn exports increased by 4% in September 2024, while ready-made garment shipments saw a robust 17% rise. Key markets for Indian cotton yarn include Bangladesh, China, and Vietnam.

India’s struggle to stay competitive in the global cotton market as domestic prices continue to exceed international benchmarks. While rising imports underscore the demand for higher-quality cotton, the reduced export volume emphasizes the need for strategic measures to balance pricing and productivity in the cotton sector.