Global Cotton Market Outlook: Demand And Production Projections 2024-2033

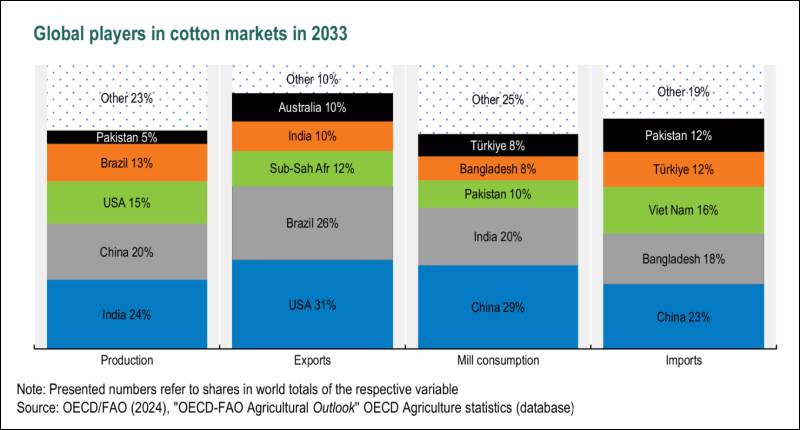

The global cotton market is set for significant growth over the next decade, driven by rising consumption and advancements in production techniques, according to OECD-FAO Agricultural Outlook 2024-2033 report. Cotton consumption is forecasted to increase by 1.7% annually, fueled by population growth and higher incomes, particularly in middle- and low-income countries. Key players in the textiles and apparel sectors, such as Bangladesh and Vietnam, are expected to see notable growth. China, already the largest cotton processing country, and India will remain pivotal in the global cotton landscape.

On the production front, lint cotton output is projected to grow at an annual rate of 1.3%, reaching 29 million tonnes by 2033. This growth will primarily be driven by yield improvements, anticipated to rise by 1.1% per year, thanks to advancements in genetics, agricultural practices and technology adoption. The production area is set to expand marginally by 0.2% annually, with Brazil and the United States leading the way in production increases.

Global trade of lint cotton is expected to rise by 2.1% per annum, reaching 12.4 million tonnes by 2033. This expansion will be driven by textile industries in countries like Bangladesh and Vietnam, which heavily rely on imports. The United States and Brazil are projected to maintain their positions as the largest exporters, benefitting from strong international demand.

Despite these positive trends, international cotton prices in real terms are expected to trend slightly downward. The market faces challenges from the competition with synthetic fibres and shifting consumer preferences. However, the growing demand for sustainable and organic cotton presents new opportunities, although it may be balanced by circular economy models like recycling and second-hand markets.

The market’s future is not without risks. Extreme weather conditions, unsustainable water usage, and pest infestations pose significant threats to yield improvements. Additionally, policy measures such as the European Union’s Product Environmental Footprint (PEF) and the Strategy for Sustainable Circular Textiles, along with geopolitical tensions, could significantly impact the market dynamics.

For the 2023-24 season, global cotton production is expected to see a slight decline compared to the previous season due to unfavourable weather conditions in key producing countries like China and India. The United States is forecasted to experience a sharp decline in production because of prolonged dry weather conditions, allowing Brazil to overtake it as the third-largest cotton producer. Conversely, global cotton consumption is projected to increase slightly, driven by higher use in Pakistan, Türkiye and Vietnam.

International cotton prices have generally declined since August 2023, influenced by weak global demand for textiles and clothing. However, the projected growth in cotton mill use, particularly in developing and emerging economies, signals a positive outlook for the market. China and India will continue to be significant consumers, with additional growth expected in Vietnam and Bangladesh due to their expanding textile industries.