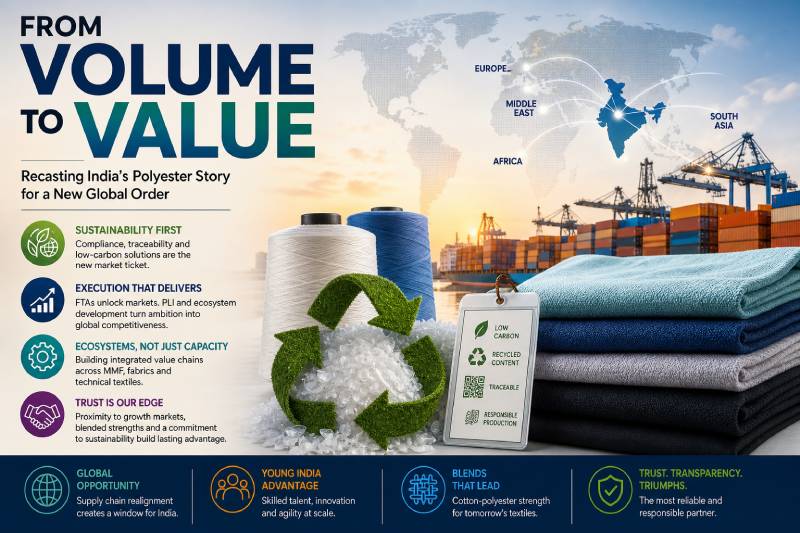

From Volume To Value: Recasting India’s Polyester Story For A New Global Order

India’s polyester story must now evolve from a narrative of cost and capacity to one of trust and relevance, writes Dr Gurudas Aras in this exclusive article

Recently, I was part of the India Polyester Conference 2026 as a panellist and dealt with various issues concerning the Indian polyester sector during the interactions. The article below is prepared based on the issues raised during the discussion, apart from my own study about the present status of the Indian polyester industry, challenges faced by it and a way forward.

India’s polyester and synthetic textile sector stands at a decisive inflexion point. For years, the narrative has revolved around capacity expansion, cost competitiveness and domestic demand strength. But the rules of the global trade game are changing—and changing fast. What will determine leadership in the next decade is not just how much we produce, but how responsibly, transparently and strategically we do so.

This article distils key insights from industry perspectives on trade shifts, policy execution and India’s long-term competitive positioning in the polyester value chain.

The New Trade Reality: Sustainability Is No Longer Optional

The most significant shift in the global trade environment today is the rapid rise of sustainability-linked regulations. Mechanisms such as carbon border adjustments and extended producer responsibility (EPR) frameworks are fundamentally reshaping how polyester and synthetic textiles are traded, priced and perceived.

These are not distant or theoretical risks—they are already influencing market access.

India, however, appears to be moving more slowly than required. While investments in feedstock security and domestic demand have been commendable, there is a visible gap in embedding:

- End-to-end traceability

- Scalable recycling infrastructure

- Low-carbon certifications

The risk is clear: Indian exports could lose competitiveness not due to cost disadvantages, but due to compliance gaps and credibility deficits. In the emerging global order, sustainability is not a branding exercise—it is a market entry requirement.

The 2030 Export Target: Ambition Meets Execution

India’s ambition of achieving USD 100 billion in textile exports by 2030 has been reiterated across policy cycles. What makes this time potentially different?

Two structural tailwinds stand out:

- Global Supply Chain Realignment

Buyers are actively diversifying sourcing away from China, creating a strategic opening for India. - Policy-Driven Ecosystem Development

Initiatives such as Production Linked Incentive (PLI) schemes and PM MITRA parks are shifting the focus from fragmented incentives to integrated scale ecosystems.

However, ambition alone does not guarantee outcomes. The credibility of the 2030 target will depend entirely on execution.

Among policy levers:

- Free Trade Agreements (FTAs) hold the highest potential impact by unlocking direct market access and improving competitiveness.

- Quality Control Orders (QCOs) present the highest execution risk. If poorly implemented, they could become compliance bottlenecks rather than quality enhancers.

The real question is not whether the target is achievable—but whether India can execute with consistency and discipline across these levers.

PLI Scheme: From Promise to Proof

The PLI scheme for textiles has transitioned from the commitment phase into execution. Its performance in the MMF (man-made fibre) and polyester segments presents a mixed picture.

On the positive side:

- Investments are flowing into higher-value MMF apparel and technical textiles

- These categories align well with global demand trends and emerging applications

However, challenges remain:

- MMF fabrics are witnessing slower-than-expected scale-up

- The scheme focuses heavily on capacity creation but does not fully address ecosystem gaps, such as:

- Raw material integration

- Skill development

- Downstream market linkages

This creates a structural disconnect between intent and execution.

Among the three PLI segments:

- Technical textiles show the strongest investment pipeline, driven by growth in sectors like healthcare and infrastructure

- MMF fabrics are the most vulnerable, with fragmented investments and slower momentum

The key takeaway is simple yet critical: The PLI scheme will succeed only if it builds ecosystems, not just capacity.

India’s True Competitive Advantage: Beyond Tariffs and Subsidies

In a world where China continues to dominate through scale, subsidies and infrastructure, India must define its competitive advantage differently—one that is structural, not temporary.

Three enduring pillars emerge:

- Markets

India’s geographical and cultural proximity to high-growth regions such as South Asia, Africa, and the Middle East provides a natural trade advantage.

- Blends

India’s unique cotton–polyester integrated ecosystem enables it to offer blended textile solutions at scale—something increasingly preferred by global buyers seeking versatility.

- Trust

Perhaps the most critical differentiator. Sustainability, traceability and innovation will define credibility in global supply chains.

India’s demographic dividend—its young and skilled workforce—further strengthens its ability to deliver flexible, design-driven manufacturing, moving beyond commoditised production.

The Road Ahead: Competing on Credibility

India’s polyester story must now evolve from a narrative of cost and capacity to one of trust and relevance.

The future will not be won by being the cheapest supplier, but by being the most reliable and responsible one.

To get there, the industry must:

- Integrate sustainability into core strategy, not as an add-on

- Align policy execution with ecosystem development

- Leverage structural strengths rather than temporary policy advantages

Conclusion

The global polyester trade is entering a new phase—one defined by accountability, transparency and strategic alignment. While China will continue to lead on scale and incentives, India has its own ingredients to lead, but leadership will depend on how quickly and effectively it adapts.

The message for the industry is clear:

India’s competitive edge will not lie in producing the cheapest polyester—but in delivering the most trusted polyester.

(Dr. Gurudas Aras is Independent Director and Strategic Advisor to leading companies in India and abroad)