China’s Cotton Imports Fall To 5-Year Low In 2022-23

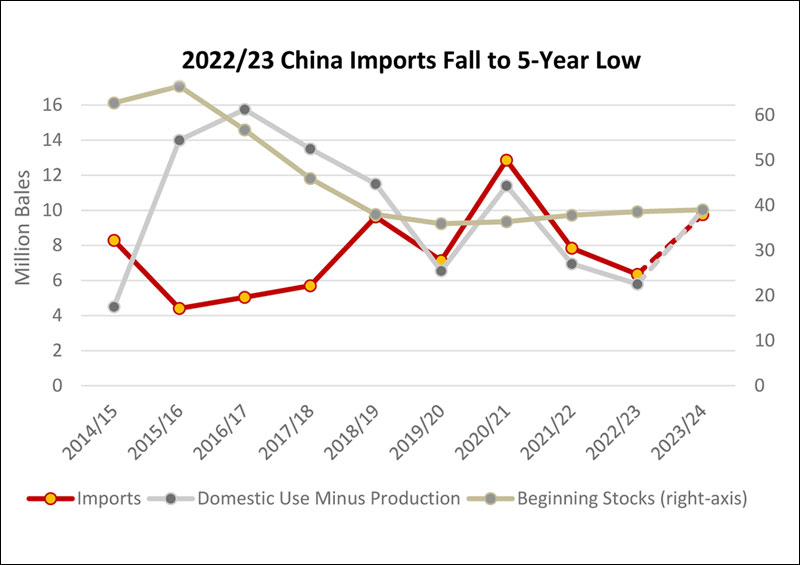

China’s cotton imports fell to their lowest level in five years, amounting to 6.4 million bales during the period of August 2022 to July 2023, which is less than half the volume witnessed two years earlier. Several factors have contributed to this decline in demand, including record-high domestic production in nine years, lower domestic prices compared to foreign markets and reduced demand for government reserves.

A significant factor driving import demand is the relative ratio of China’s domestic use to production. This has become increasingly crucial as stocks have significantly dropped from historic levels nearly a decade ago. The country’s latest crop marked a considerable increase of approximately 4.0 million bales compared to the previous year, reaching 30.7 million bales, while domestic use is forecasted to be slightly below the 5-year average at 36.5 million bales. Moreover, the beginning stocks of domestic cotton in Xinjiang warehouses surpassed the previous year by over 6.0 million bales, further impacting import demand and leading to an upswing in domestic lint spinning.

The demand for imports was further restrained by the considerably higher prices of imported cotton relative to domestic options. At the beginning of the marketing year, the domestic cotton price was nearly 40 cents lower than imports, presenting a stark contrast to the previous year when China’s domestic cotton price was over 10 cents higher than the customs cleared A-Index.

China’s state reserves of foreign cotton are perceived to be at a high level after three consecutive years of large purchases, with most of these reserves originating from the United States. This is attributed to the government’s continuous efforts to replenish state reserves. Notably, over half of China’s U.S. cotton imports since the Phase One Agreement are likely still in state warehouses or under government control, in contrast to imports channeled for domestic use. During the first ten months of the marketing year, the United States supplied over half of China’s imports, marking the highest market share in nearly 15 years.

Looking ahead, imports for the 2023-24 marketing year are forecasted to rise by 3.4 million bales, reaching 9.8 million bales. Meanwhile, China’s domestic cotton production is projected to fall by over 3.7 million bales to 27.0 million, and beginning stocks for commercial enterprises are expected to be lower than the previous year’s robust level. The potential for greater sales of imported cotton from government reserves is expected to drive higher imports and aid in replenishing state inventories.