T&A Industry 2026: India Balances Growth And Global Shifts

The global textile and apparel (T&A) industry entered 2026 at a critical inflection point, shaped by geopolitical realignments, tariff disruptions, cautious consumer demand and accelerating supply-chain diversification. According to Wazir Advisors, the global apparel market is estimated at US$ 1.9 trillion in 2025 and is projected to grow to US$ 2.3 trillion by 2030, reflecting a moderate 4 percent CAGR, as brands balance cost pressures with sourcing resilience.

Against this backdrop, India’s textile and apparel industry continues to demonstrate resilience, anchored by a large domestic market, policy support and a gradual shift toward higher-value segments.

Global textile and apparel trade was estimated at US$ 900 billion in 2025, growing at a CAGR of 3 percent since 2020, with apparel accounting for nearly 60 percent of total trade. However, the year 2025 was marked by sharp disruptions, particularly following the introduction of higher, country-specific tariffs by the United States.

China, while remaining the world’s largest exporter with a 32 percent global trade share, witnessed a significant erosion in competitiveness. United States apparel imports from China declined sharply post-tariff implementation, while Vietnam emerged as the largest supplier to the U.S., increasing its market share to over 21 percent. India, despite a strong start to the year, saw export momentum slow sharply after August 2025, highlighting its vulnerability to sudden policy shocks in key export markets.

The developments reinforced a broader structural shift underway, global buyers are actively reducing dependence on single-country sourcing models and prioritising supplier flexibility, compliance readiness and speed-to-market over scale alone.

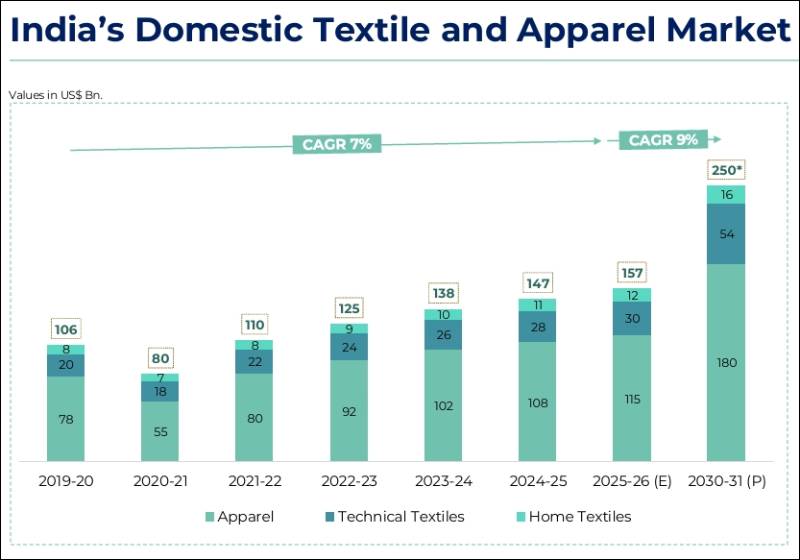

India’s textile and apparel market is estimated at US$ 194 billion in 2025–26, registering a year-on-year growth of 5 percent. The domestic market continues to dominate, contributing nearly 80 percent of total industry size, while exports account for the remaining 20 percent.

Within the domestic segment, apparel remains the largest contributor at US$ 115 billion, followed by technical textiles at US$ 30 billion and home textiles at US$ 12 billion. Strong consumption in Tier-2 and Tier-3 cities, expanding organised retail and rising preference for branded apparel have helped cushion the impact of weak export demand.

India’s domestic T&A market has grown from US$ 106 billion in 2019–20 to US$ 157 billion in 2025–26, reflecting a CAGR of 7 percent. To achieve the government’s ambitious US$ 250 billion domestic market target by 2030–31, the industry will need to accelerate growth to nearly 9 percent annually, supported by investments, productivity improvements and formalisation.

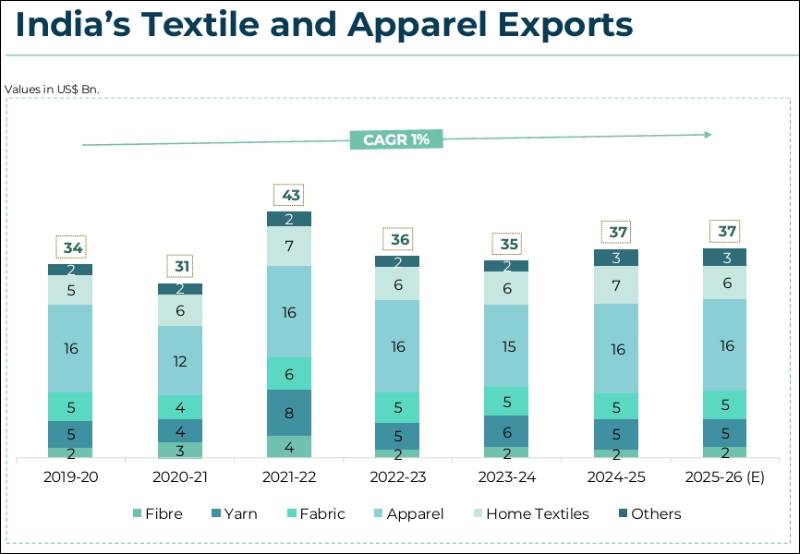

India’s textile and apparel exports stood at US$ 37 billion in 2025–26, showing flat growth compared to the previous year. Apparel continues to account for the largest share at around 45 percent, followed by textiles including yarn, fabric and home textiles.

Export performance has remained muted since 2019–20, with a modest CAGR of just 1 percent. Achieving the Ministry of Textiles’ US$ 100 billion export target by 2030–31 will require a sharp acceleration to a 17 percent CAGR, necessitating deeper integration into global value chains, faster FTA implementation and stronger man-made fibre (MMF) capabilities.

State-wise, Tamil Nadu remains India’s largest T&A exporter with shipments worth US$ 8.22 billion, followed by Gujarat (US$ 5.94 billion), Haryana, Maharashtra and Uttar Pradesh, underlining the geographic concentration of export-oriented manufacturing.

India’s production landscape is undergoing a gradual transformation. While cotton continues to dominate fibre production, accounting for 38 percent of total output, the fastest growth has been recorded in polyester staple fibre and man-made filament yarn, reflecting changing global demand patterns.

Man-made filament yarn production has grown at a CAGR of 23 percent since 2019–20, even as exports declined and imports increased, signalling strong domestic consumption. Similarly, synthetic garment exports have grown at a CAGR of 9 percent, outpacing cotton garments, which reinforces the urgency for India to strengthen MMF-based value chains.

The year 2025 witnessed renewed investment momentum in the sector, with MoUs exceeding Rs 27,400 crore, driven by capacity expansion, modernisation and diversification into MMF and technical textiles. Progress under the PM MITRA mega textile parks initiative is expected to play a pivotal role in creating integrated, plug-and-play manufacturing ecosystems.

Policy measures such as GST rationalisation, extension of RoDTEP and RoSCTL incentives, deferment of select Quality Control Orders and customs duty relief on raw cotton have eased cost pressures and improved operational viability for manufacturers.

At the same time, the National Technical Textiles Mission, backed by an outlay of Rs 1,480 crore, continues to support R&D, innovation and export promotion in high-performance textile segments.

Looking ahead, demand conditions in 2026 are expected to remain cautious and uneven, with global brands continuing to place short-term and fragmented orders. Rising compliance requirements, sustainability mandates and traceability norms will raise the cost of participation, making scale alone insufficient for competitiveness.

However, India stands to benefit from the expected ratification of the India–UK FTA and the proposed India–EU FTA, alongside recently concluded agreements with EFTA countries, Oman and New Zealand. These trade pacts could significantly enhance market access and tariff parity for Indian exporters.

With domestic demand acting as a stabiliser, PLI-led investments accelerating MMF and technical textile capacities, and supply-chain diversification working in India’s favour, the industry enters 2026 with cautious optimism, but success will hinge on execution, agility and speed.

(Source: Wazir Advisors Report)