US Tariffs Weigh on India’s Apparel Exports, ICRA Sees Recovery Ahead

India’s apparel exports recorded a modest growth of 1.5% year-on-year in USD terms during the first 10 months of FY2026, as US tariff pressures continued to dampen demand, according to a latest report by ICRA. A depreciating rupee, however, supported relatively stronger growth of 5.8% in INR terms.

Exports to the US declined by around 6% in USD terms during the period, reflecting the impact of tariff-led demand contraction. This was partially offset by increased shipments to alternative markets such as the UK and the UAE.

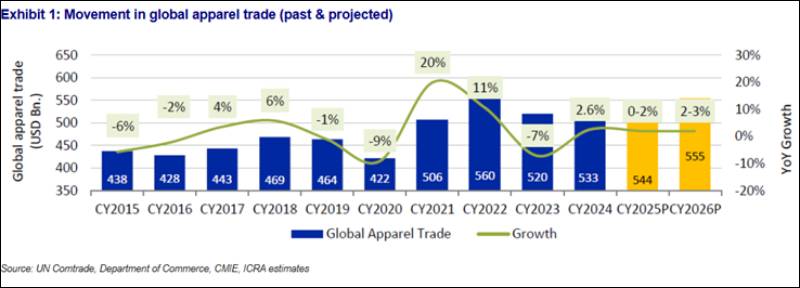

Globally, apparel trade is estimated at approximately $550 billion, with the US and Europe accounting for nearly half of total imports. While imports into Europe grew by 5–6% year-on-year in the first 11 months of CY2025, driven by nearly 9% growth in the EU due to retailer restocking US import volumes declined by 3-4% amid tariff headwinds.

India’s apparel exports stood at around $16 billion in FY2025, accounting for nearly 3% of global trade. The US and Europe (including the EU and the UK) remain key markets, contributing approximately 32–33% and 31–32% shares, respectively.

ICRA revised its outlook on the Indian apparel export sector to Stable from Negative in February 2026, supported by easing tariff pressures and expected gains from potential free trade agreements (FTAs) with the EU and the UK.

Looking ahead, the agency expects apparel exporters’ revenues to grow by 8–11% year-on-year in FY2027, with operating margins likely to improve by around 200 basis points to approximately 9.5%.

However, geopolitical risks particularly in West Asia, remain a key monitorable. Around 8% of India’s apparel exports are directed to the UAE, with higher exposure to the broader West Asian region. Any prolonged disruption in critical shipping routes such as the Strait of Hormuz or the Red Sea could delay shipments, necessitate rerouting, and elongate the cash conversion cycle.

The report also noted that while capital expenditure is expected to remain subdued in FY2026, a moderate uptick is likely in FY2027, supported by potential FTA formalisation with the UK and the EU. However, uncertainty around the US tariff environment may continue to discourage large, debt-funded expansions.

Credit metrics are projected to improve in FY2027, with interest coverage expected to rise to around 4.6 times from 3.3 times in FY2026, while total debt to OPBDITA is likely to moderate to approximately 2.3 times from 3.3 times.