USDA: 2023/24 Global Cotton Use Forecast At 3-Year High

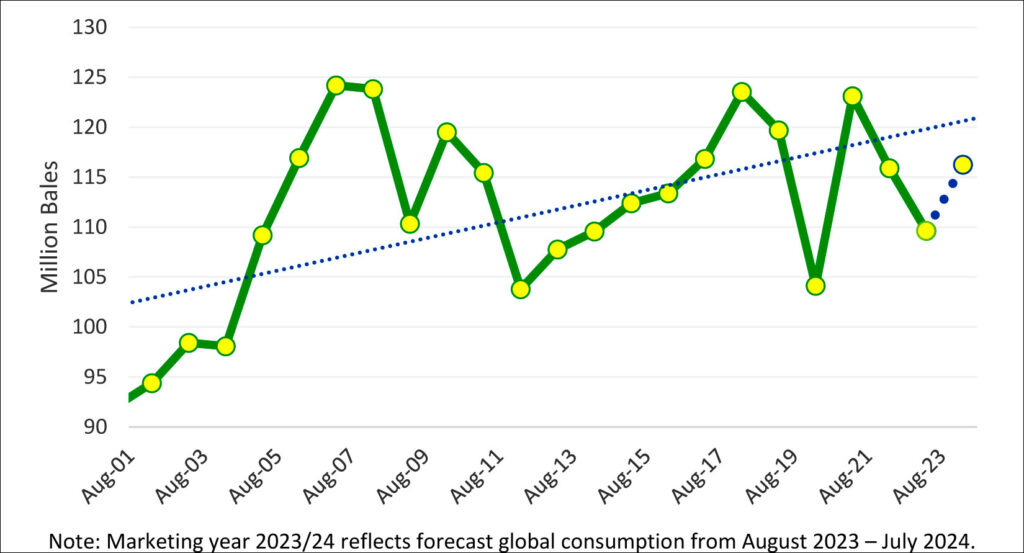

Global cotton consumption is forecasted at 116.2 million bales, up more than 6.6 million from the previous year. Greater cotton supplies, lower producer price inflation, low global cotton yarn stocks, and greater margins for spinners are expected to boost future use. Consumption is forecast at the second highest level in 5 years and implies an annual growth rate of 6.0 percent, significantly higher than the long-term annual average of 1.5 percent since 1960/61. Still, consumption is projected below trend as macroeconomic headwinds and competition from chemical fibers continue to pressurize global use.

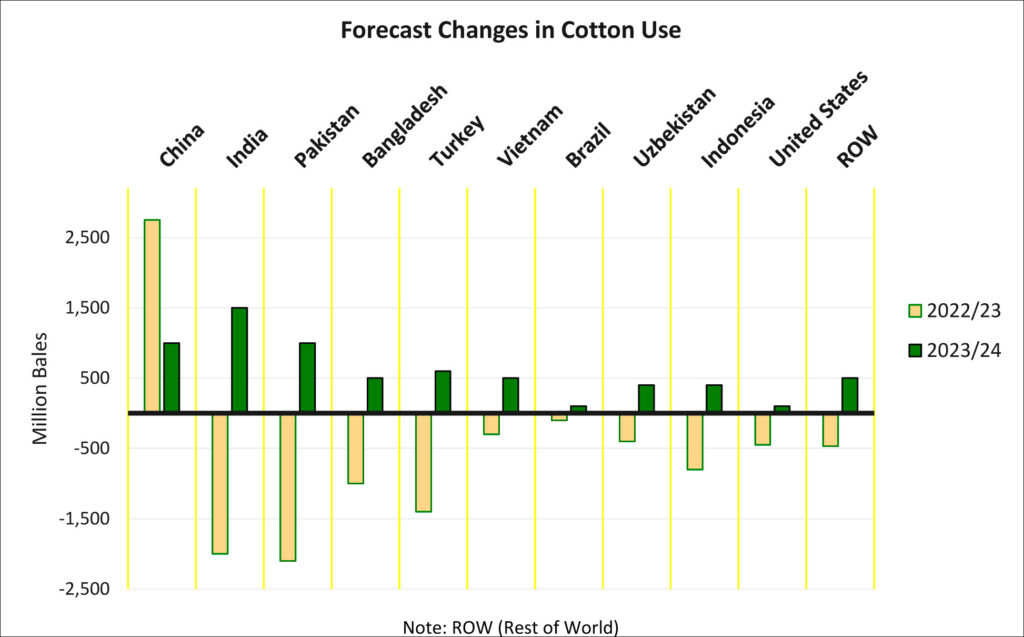

The world’s three largest consumers – China, India, and Pakistan – are forecast to account for more than half of the global increase. Of the top ten consuming countries, all are expected to have higher use. After significant reductions for India, Pakistan, and Bangladesh in the previous year, a general easing of financial pressures and greater supplies are expected to support consumption. Prospects for a depreciating U.S. dollar, greater access to opening letters of credit, and lower energy costs are expected to boost growth.

Higher cotton consumption is also supported by prospects for global economic growth. Cotton lint consumption and year-over-year changes in global Gross Domestic Product (GDP) are mostly correlated, however, cotton use and GDP do not always follow the same trend as illustrated in the chart alongside. The April 2023 World Economic Outlook published by the International Monetary Fund (IMF) projects global GDP to grow 2.8 percent for calendar year 2023 and 3.0 percent for 2024. The IMF’s outlook is uncertain and mentions concerns in the global banking sector, persistently high consumer inflation, and other factors that may inhibit global growth. Recent global cotton consumption relative to global gross GDP and population remains significantly below the level of record consumption witnessed more than 16 years prior. Since the 2006/07 consumption record of more than 124.0 million bales, competition with man-made fibers and macroeconomic challenges have pressured not only the level but the volatility of consumption.

Higher cotton yarn prices compared with cotton lint (roughly half of input costs) supports greater profit margins. Year-to-year changes in this margin (cotton yarn minus lint) have trended closely with changes in global cotton consumption as seen alongside. A less volatile and average level going into 2023/24 is expected to support greater consumption compared with the previous year’s low expected margins. China’s yarn is used to represent global yarn price as it is the largest cotton yarn producer, importer, and consumer. Comparing the yarn price across various origins of cotton lint is a general gauge for capturing spinner’s profitability in and outside China.

Another factor driving higher consumption is expected low inventories across the cotton product supply chain at the beginning of 2023/24. Disrupted and delayed shipments of consumer goods in calendar years 2021 and 2022 inflated global inventories and retailers responded with unusually large reductions in 2022/23 product orders. In addition, China’s lockdown orders starting in early 2022 also slowed consumption to unusually low levels. Global mills’ operating rates have improved and are expected to continue into 2023/24 relative to the previous year. As the effects of the pandemic further recede, inventory levels across the cotton product supply chain are expected to normalize and support higher use. Rising household savings accumulated during China’s COVID lockdowns are also expected to support greater domestic purchases of cotton finished goods in one of the world’s most populous countries. Uncertainties in the consumption outlook include the level of global cotton production, a persistent shift of consumer purchases to services and away from goods, and the unexpected impacts of global financial tightening in response to persistently high inflation. The ongoing Russian invasion of Ukraine has further contributed to uncertainty regarding global economic growth. This is particularly acute for Europe, as both the European Union and United Kingdom are the world’s largest buyer of consumer products made from cotton fiber.

2023/24 Outlook

Production is mostly unchanged at 116.2 million bales, 300,000 lower compared with the previous year as declines in China and Turkey are mostly offset by larger crops in the United States and Pakistan. The small change in global production is partially due to less competitive prices for cotton relative to other crops but this is offset by more favorable expected weather in major producing countries.

In January 2023, the A-Index was about one-third lower than a year prior relative to U.S. Gulf corn prices and Rotterdam U.S. soybean prices, contributing to lower plantings of cotton across major producing countries. Despite lower plantings, harvested area in the United States is expected to rise as less acres are abandoned compared with the previous year’s record level. Greater production is also expected in Pakistan where unusually severe rainfall and flooding drove the previous year’s crop to the lowest level since 1983/84.

Global trade is forecast up roughly 5.0 million bales from the previous year to 42.8 million as higher exportable supplies and global consumption are expected to support greater world trade. China is projected to be the largest importer at 9.0 million bales after last year’s decline to 6.8 million. The country’s demand is expected to rise 1.0 million, owed to stronger private mill demand, higher prices for domestic cotton relative to imports, and supplies for state reserves. Of the top five importers, all are expected to witness growth due to greater consumption.

Global ending stocks are mostly unchanged at 92.4 million bales. Despite higher global consumption, drastically higher carry in is projected to cap any significant fall in stocks. Stocks are projected above the 5-year average and are expected to prevent any significant rise in global cotton prices. The U.S. season average farm price for 2022/23 is forecast at 78 cents, down 4 cents from the previous year.