India To Become Net Cotton Importer Amid Declining Production: USDA Report

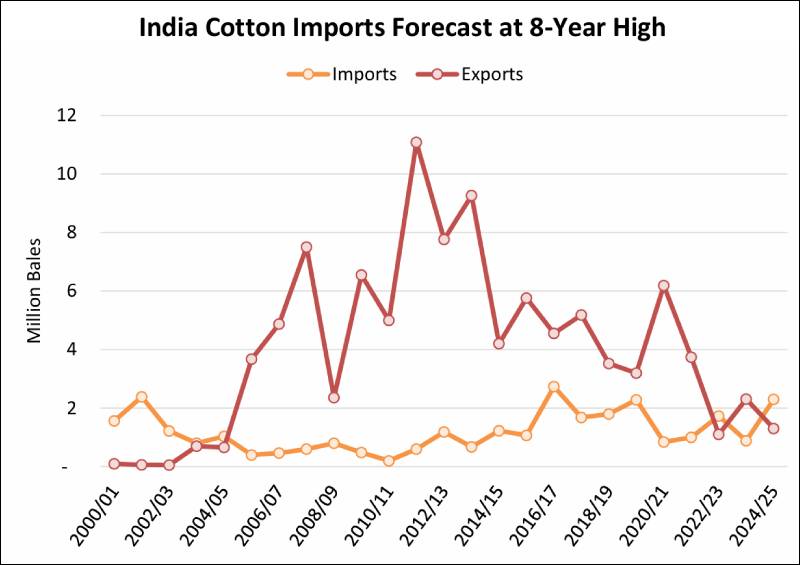

India is expected to become a net importer of cotton for only the second time in two decades, as cotton imports for the 2024/25 marketing year (August 2024 – July 2025) are forecast to reach 2.3 million bales, nearly triple the previous year’s figure, according to a recent report by the U.S. Department of Agriculture (USDA). At the same time, exports are projected to decline by 1.0 million bales to 1.3 million, reflecting lower domestic production, strong mill demand and elevated domestic prices.

India’s cotton production is expected to shrink by 7% to 24.0 million bales in 2024/25, marking the lowest output in 15 years. A severe heatwave in Northern India hampered planting activities, while farmers, attracted by more lucrative prices for rice and pulses, diverted land away from cotton cultivation. This trend persisted despite the government raising the Minimum Support Price (MSP) for seed cotton by 7%. Lower production will further squeeze exportable supplies, already impacted by reduced carryover stocks from the previous season.

Domestic mill use is forecast to rise by 500,000 bales to 25.5 million, the highest level in four years, further increasing reliance on imports. Mills are expected to benefit from the tariff removal on extra-long staple (ELS) cotton, implemented in February 2024, which has incentivized the import of both ELS and upland varieties. Cotton lint prices in India, currently hovering around 87 cents per pound with a 20-cent basis premium, have made imports an attractive option.

Imports from the United States have surged, with total commitments nearly six times higher than the previous year, according to U.S. export sales data. The increase highlights robust demand for both ELS and upland cotton to supplement domestic supplies. Brazil has also expanded its market share in India, shipping nearly twice the amount of cotton in August and September 2024 compared to the entire 2023/24 season.

India’s cotton exports are projected to decline to 1.3 million bales due to lower production and higher domestic prices, reducing competitiveness in global markets. While international cotton prices have fallen, India’s increased MSP has further narrowed margins for exporters.

The decline in exports may affect India’s cotton yarn shipments to key markets such as Bangladesh and China, which typically purchase significant volumes from India. Historically, higher domestic cotton prices have reduced India’s yarn exports, especially when China’s spot prices are more favourable.

On the global front, USDA projects a mixed cotton outlook. While global production is expected to rise slightly to 116.6 million bales, driven by gains in China and Brazil, U.S. production is forecast to fall by 300,000 bales following Hurricane Helene’s damage in North Carolina and Georgia.

Global cotton consumption is expected to remain flat at 115.7 million bales, with increased use in Bangladesh offsetting declines in the U.S., where mill activity continues to shift to central America. Global trade is set to drop by over 500,000 bales to 42.5 million, with China reducing imports by 500,000 bales. Global ending stocks are forecast to decrease to 76.3 million bales, driven by higher consumption in China.

India’s shift toward becoming a net importer reflects the evolving dynamics within its cotton industry, driven by reduced production, heightened domestic demand and challenging export conditions. With domestic supplies under pressure, India’s textile sector is likely to rely heavily on imports throughout the season.

The situation will also have implications for India’s exports of cotton yarn and textiles, with global demand from Bangladesh, China and western markets playing a pivotal role in shaping industry performance through the 2024-25 marketing year.