Brazil Cotton Exports & Closing Stocks To Reach Record High In 2025/26: USDA Report

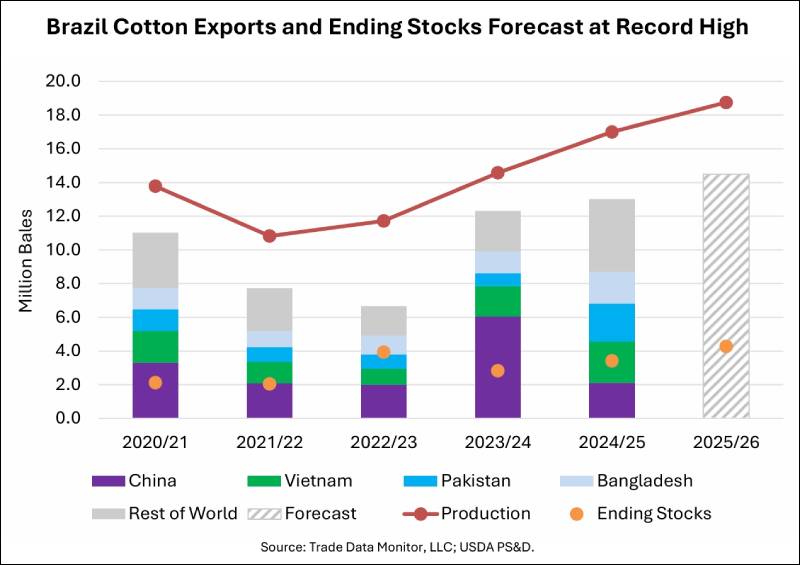

Brazil’s cotton sector is set for another landmark year, with exports forecast to reach a record 14.5 million bales in marketing year 2025/26 (August–July), up 1.5 million bales from the previous season. If realized, this would mark the third consecutive year of record-breaking shipments, reinforcing Brazil’s position as a dominant force in the global cotton trade.

The surge in exports has been underpinned by rapid production growth, driven by both higher harvested area and improved yields. However, export gains have not kept pace with output expansion, while domestic consumption has remained largely unchanged. As a result, ending stocks are projected to climb to a record 4.3 million bales in 2025/26, the third straight annual increase.

Abundant supplies have weighed on domestic prices over the past three years, mirroring softer global trends.

In the first half of 2025/26, Brazil’s cotton exports rose 6 per cent year-on-year, with notable gains in shipments to China, Bangladesh, Turkey and India.

China has reclaimed its position as the top destination, with year-to-date shipments already surpassing the total volume exported to the country in 2024/25. However, volumes remain well below 2023/24 levels, when China was actively replenishing state reserves.

Vietnam, which was the leading importer of Brazilian cotton last season, has sharply reduced purchases this year, increasing imports from the United States instead.

December 2025 marked a record monthly export volume, demonstrating the industry’s ability to manage logistics amid surging output. Exporters have also diversified port usage following previous congestion at Santos. In the first half of 2025/26, nearly 10 per cent of shipments moved through ports other than Santos, more than double the five-year average of 4 per cent.

Looking ahead, Brazil’s National Supply Company (CONAB) has projected a smaller 2026/27 crop, citing expectations of lower yields and reduced planted area due to high input costs and subdued cotton prices. Nevertheless, elevated carryover stocks could cushion any potential impact on export volumes.

Globally, cotton production is forecast to rise 425,000 bales to 119.9 million, as a larger crop in China offsets reduced output in Argentina.

Global consumption, however, is projected to decline 200,000 bales to 118.7 million, reflecting weaker demand in Pakistan, Indonesia, Portugal and Thailand. While production is up nearly 1 per cent year-on-year, consumption remains flat, keeping market fundamentals relatively balanced.

World trade is expected to hold steady at 43.7 million bales. Lower exports from the United States and Argentina are likely to be offset by higher shipments from Australia. On the import side, reduced buying by Pakistan, Turkey, and select Southeast Asian nations is balanced by stronger demand from China and India.

Global ending stocks are forecast to increase by over 600,000 bales to 75.1 million, with higher inventories in China, India and the United States more than compensating for stock declines in Australia, Pakistan and Turkey.

Meanwhile, the U.S. season-average farm price for 2025/26 is projected to ease by 1 cent to 60 cents per pound, reflecting ample global supplies and subdued demand growth.

With record exports and swelling inventories, Brazil remains at the centre of global cotton dynamics, even as softer demand and price pressures shape the outlook for the coming seasons.