Australia Strengthens Position As Global Cotton Trade Dynamics Shift

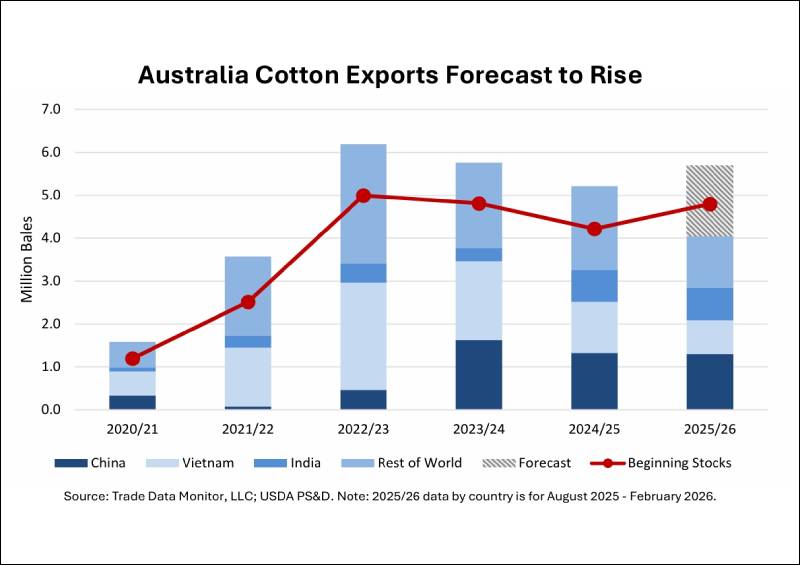

The global cotton landscape is undergoing a significant realignment, with Australia emerging as a central player. Since the 2022-23 marketing year, Australia has consistently ranked as the world’s third-largest cotton exporter, trailing only Brazil and the United States. This trajectory is set to continue as exports are forecast to rise nearly 10 per cent to 5.7 million bales in the 2025-26 marketing year.

The current surge in Australian exports is particularly notable because it occurs despite a forecast for lower domestic production. The market is being sustained by high opening stocks from a massive 2024-25 harvest, which are supplying international buyers until the new crop is harvested at the end of the current marketing year. Australia’s unique harvest cycle as a Southern Hemisphere producer, harvesting in April and beginning exports in May, means that late-season trade will begin to reflect this smaller 2025-26 crop.

Geopolitical shifts have fundamentally redrawn Australia’s export map. After two years of limited trade with China due to political tensions, the relationship has reversed. China has eased restrictions and resumed significant purchases, now accounting for one-third of all Australian cotton shipments. This return to the Chinese market has displaced U.S. cotton, which has subsequently seen its shipments to Vietnam rise, in turn displacing Australian market share there. Meanwhile, India has emerged as a critical partner following the removal of cotton duties in late 2025. Indian imports of Australian fibre have surged to record levels, already surpassing last year’s totals.

Despite this growth, the concentration of Australian trade presents a distinct vulnerability. Currently, 70 per cent of Australia’s year-to-date exports go to just three markets: China, Vietnam and India. This high level of market concentration leaves the Australian sector more exposed to geopolitical shocks than its major competitors, Brazil and the United States, whose top three markets account for less than 60 per cent of their total exports.

On a global scale, the outlook for 2025-26 is one of expansion. Total world production is forecast at 121.9 million bales, driven by larger crops in China, India and Pakistan. Global consumption is also rising, projected at 119.1 million bales as robust demand in China and India offsets lower activity in Bangladesh and Vietnam. As trade flows continue to stabilize, the U.S. season-average farm price is forecast at 61 cents per pound, reflecting a market that is actively adapting to these new regional dominance patterns.