Geopolitics Hits Textile Sentiment: ITMF

The International Textile Manufacturers Federation (ITMF) has released the findings of its 37th Global Textile Industry Survey (GTIS) conducted in March, highlighting a sharp deterioration in industry sentiment as geopolitical tensions disrupt global markets.

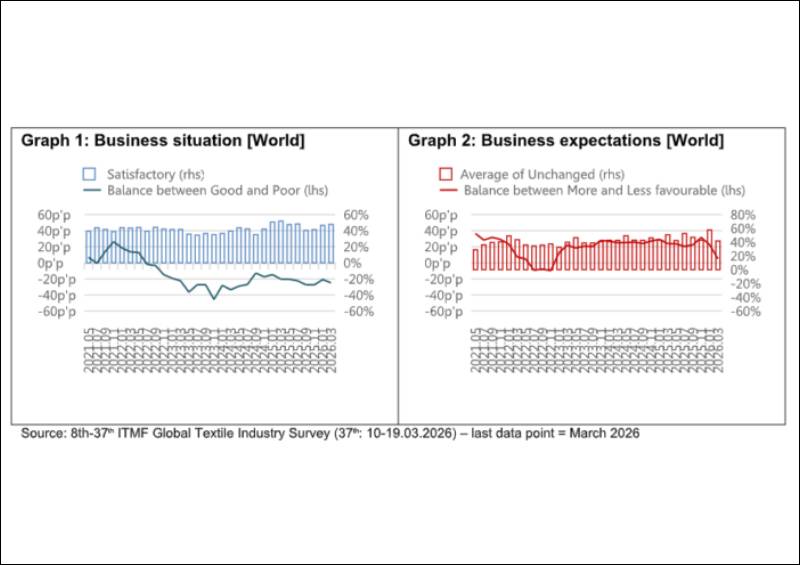

According to the survey, the overall global business climate has weakened significantly, with the business situation balance plunging to -25 percentage points. The downturn is largely attributed to escalating geopolitical conflicts, particularly the US/Israel-Iran war, which has triggered volatility in energy markets and heightened uncertainty across supply chains.

Regionally, Africa stood out as the only area reporting a positive business environment, while North and Central America experienced the steepest decline. Across industry segments, garment manufacturers demonstrated relative resilience, whereas textile machinery producers continued to face deeply negative conditions.

Business expectations have also taken a hit, with the global outlook balance dropping sharply from over +23 percentage points to just +5 percentage points, the lowest level recorded since November 2022. The findings renewed stagflation concerns, drawing parallels with the economic disruptions seen after the Russian invasion of Ukraine.

In terms of regional outlook, South America emerged as the most optimistic, while South-East Asia reflected the highest levels of pessimism. Among industry players, brands and retailers expressed the most confidence, contrasting with a notably weak outlook among weavers and knitters.

A key shift highlighted in the survey is the rise of geopolitics as the industry’s primary concern for the first time, cited by 50% of respondents. This narrowly surpasses weak demand, which was noted by 49%. The growing concern is driven by the ongoing conflict in Iran, escalating energy costs, rising raw material prices and logistical disruptions, particularly around the Strait of Hormuz.

Interestingly, tariffs have become less of a concern, dropping sharply from 31% to 13%. In response to the evolving landscape, companies are increasingly focusing on diversifying markets beyond the US and absorbing costs internally, while large-scale strategies such as production relocation and capital-intensive investments remain limited.