Indian Home Textile Industry Poised for 8-10% Growth In FY25

The global home textile industry, valued at USD 122 billion in 2023, is projected to reach USD 134 billion by the end of 2024 and grow at a CAGR of 5-5.5% to approximately USD 185 billion by 2030. China leads in home textile exports, followed by India and Turkey, with the USA being the largest importer of these products.

In India, the home textile industry, comprising six major listed companies accounting for about 65% of the domestic market, is expected to grow by 8-10% in FY25, with operating margins (PBILDT) remaining between 14-15%. Growth will be driven by rising per capita income, urbanization, the booming real estate sector, and increased consumer awareness of hygiene. After facing setbacks in FY23, the industry is on a recovery path, evident from FY24 performance.

The financial strength of the major players remains robust, supported by capacity expansion plans and healthy balance sheets.

Global Home Textile Industry Overview

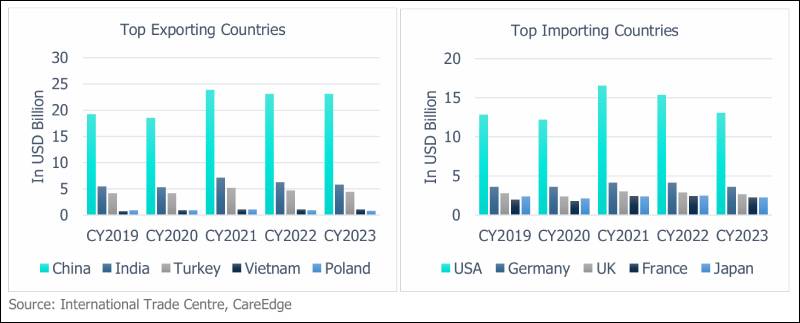

In 2023, the global home textile market accounted for 7-8% of the overall textile sector. China remains the top exporter with USD 23 billion in exports in 2023, followed by India with USD 5.7 billion, and Turkey with USD 4.2 billion. During the COVID-19 pandemic, India’s exports peaked at USD 7.1 billion due to increased demand from the US and Europe, driven by the China+1 strategy.

The USA is the largest importer, making up 30% of global home textile imports, with China supplying 35% and India 29%. India’s exports grew 12.27% between 2019 and 2023, while China’s dropped by 13.2%, reflecting a shift toward India. In the UK, India faces stronger competition, with China leading at 23% of imports, followed by Pakistan at 20% and India at 10%.

Indian Home Textile: Sustaining Growth

India holds 7-8% of the global home textile market and ranks among the top suppliers to the US. Major export categories include carpets, rugs, furnishing articles, bed linen, and kitchen/table linen.

The home textile sector experienced steady growth from FY16 to FY20, with a notable surge during the pandemic. FY21 saw a 13% year-over-year (YoY) growth, followed by a 26% YoY increase in FY22, driven by pandemic-related demand and the China+1 strategy. However, by Q3 FY22, the industry faced challenges such as increased raw material costs and freight charges. Additionally, economic conditions in the USA and Europe and rising energy costs in the EU contributed to a 12% YoY decline in exports in FY23.

Despite these challenges, the industry began to recover in FY24, particularly in the US market, where increased demand contributed to a notable improvement.

Raw Material Price Trends: Impact on Profitability

Cotton, the main raw material for bed linen, plays a crucial role in the profitability of home textile companies. In June 2022, cotton prices reached ₹1,00,000 per candy (₹272 per kg) due to poor crop yields. However, prices corrected in December 2022, stabilizing at ₹160-₹164 per kg. Additionally, freight costs have remained a challenge. Shipping expenses surged during the Russia-Ukraine war, and the Red Sea crisis in 2024 further inflated costs, as rerouted vessels increased transit times and logistics expenses.

Financial Performance and Recovery

In FY22, the Indian home textile industry saw a 37% increase in total operating income (TOI), driven by exports to the US and Europe, along with better price realizations. Operating margins peaked at 17%. However, post-FY22, demand waned, particularly in the Western markets, leading to a 491-basis point drop in margins, bottoming out at 9% in Q2 FY23. Factors such as higher cotton inventory costs, freight charges, and reduced discretionary spending in key markets contributed to the decline.

Nevertheless, by Q3 FY23, the sector began showing signs of recovery, supported by rising domestic demand and an uptick in exports.