India’s GCC Expansion Hits Record 31 Mn Sq Ft; Metros Lead Growth: JLL Report

India’s Global Capability Centres (GCC) leasing activity reached a record 31 million sq. ft in 2025, reflecting the evolution of a sophisticated ecosystem of specialised metropolitan hubs, each commanding distinct competitive advantages across critical industry verticals.

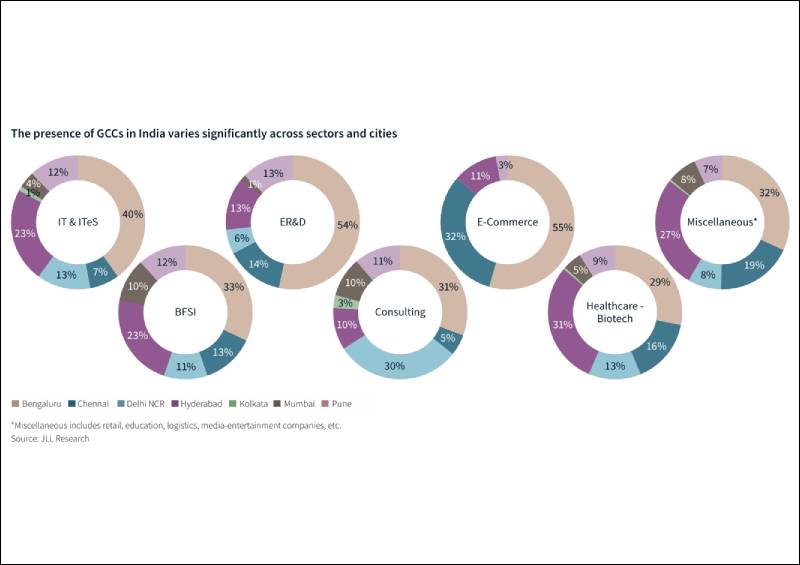

According to a latest JLL (Jones Lang LaSalle) report titled ‘India GCC Guide 2025’, the top six major cities have strategically positioned themselves as GCC powerhouses across a diverse spectrum but with unique offerings to specific sectors.

Bengaluru commands a 34-39 per cent market share through its over 900 GCC units, setting the benchmark as the leader of the pack, while Hyderabad’s 20-23 per cent market capture is built upon its status as the undisputed leader of the healthcare-biotech sector. This geographic specialisation model is reshaping how multinational corporations approach their Indian operations, moving beyond simple cost arbitrage to leverage each city’s unique strengths.

“India’s GCC landscape has evolved, moving beyond simple cost arbitrage to leverage each city’s unique strengths. The numbers tell a compelling story of sustained growth and maturation. With over 90 per cent of current GCC activity concentrated in Tier I cities, these centres have commanded more than 263 million sq ft of Grade A office stock across the top seven cities, while driving 40 per cent of all office leasing activity over the past decade. What we are witnessing is not just expansion but acceleration,” says Samantak Das, Chief Economist and Head of Research and REIS, India, JLL.

“Over 200 new GCCs have entered India in just last two years, with projections indicating total GCC footprint will surpass 350 million sq. ft within the next 3-4 years. This growth is particularly driven by US-headquartered firms, which represent 70% of all GCC demand from 2018 to 2025, underscoring India’s strategic importance to American enterprises. The future belongs to GCCs that view location strategy not as a cost centre, but as a competitive differentiator, leveraging India’s multi-tiered city framework to build resilient, scalable operations that can adapt to changing global business demands. This multi-year growth trend reflects a fundamental shift where India has become indispensable to global corporate strategy, offering not just operational efficiency but strategic capability building across the entire value chain,” adds Das.

Bengaluru has solidified its position as India’s undisputed GCC capital. Bengaluru continues to dominate India’s GCC ecosystem, with the Silicon Valley of India now hosting over 900 GCC units, leveraging its robust talent pipeline, mature business ecosystem, and established tech credentials. The city’s strength spans IT/ITeS, research and development across engineering and manufacturing sectors, innovation centres spearheading cutting-edge analytics, and retail operations, making it the preferred destination for companies seeking comprehensive offshoring capability development.

“Bengaluru continues to solidify its position as India’s undisputed GCC capital, with over 900 GCC units now operating in the city. The city’s commanding 34-39% market share is built on its robust talent pipeline, mature business ecosystem, and established tech credentials. Bengaluru’s comprehensive strength across IT/ITeS, research and development, innovation centres, and retail operations makes it the preferred destination for companies seeking world-class offshoring capability development,” says Rahul Arora, Head – Office Leasing & Retail Services, Senior Managing Director (Karnataka, Kerala), India, JLL.

According to the global property consultancy firm report, Hyderabad has emerged as healthcare-biotech leader. The city has captured 20-23 per cent of India’s overall GCC market, establishing itself as the country’s premier destination for healthcare and biotechnology operations. The city’s strategic advantages include world-class infrastructure, government policy incentives, and a rapidly growing talent pool specialising in BFSI and analytics as well. Key growth sectors include IT/ITeS, semiconductors, biotechnology, pharmaceuticals, and life sciences, positioning Hyderabad as a critical hub for innovation-driven enterprises.

Pune has secured 15-20 per cent of the national GCC activity over the past four years, attracting major multinational corporations through superior quality-of-life metrics, talent availability and strategic sector positioning. The city excels in BFSI, automotive, IT/ITeS, manufacturing, and engineering services. Similarly, Chennai has experienced strong demand growth year-over-year since 2023, cementing its status as India’s manufacturing and automotive hub with complementary strengths in IT/ITeS, BFSI, and Engineering Research & Development (ER&D) built on its STEM talent base.

Delhi NCR has evolved into a corporate services powerhouse, capitalising on its diverse economic base and strong growth momentum. The region demonstrates strength in IT, BFSI, e-commerce and retail, healthcare, consulting, and education sectors. Mumbai, as India’s commercial capital, continues to attract strategic capability and solutions centre set-ups driven by major banks, financial institutions and multinational corporations, with BFSI continuing to remain its primary sector of excellence.

While Bengaluru, Hyderabad and Pune with the other major metros have long dominated the landscape, a shift is underway as global enterprises discover the untapped potential of India’s Tier II cities, says the report.

As India’s GCC landscape continues to evolve, organisations that embrace strategic geographic diversification will be best positioned to capitalise on the country’s vast talent ecosystem while optimizing operational efficiency. The future belongs to GCCs that view location strategy not as a cost centre, but as a competitive differentiator, leveraging India’s multi-tiered city framework to build resilient, scalable operations that can adapt to changing global business demands.