India’s T&C Exports: Cotton Surges, While Apparels Decline!

In the dynamic world of India’s textile and clothing (T&C) sector, the fiscal year 2023-24 has brought both challenges and opportunities. As global markets shift and consumer preferences change, India’s role in the global textile trade is closely examined. This analysis, written by Henry Dsouza, Associate Editor of Textile Insights, explores the trends that shaped India’s T&C exports. From strong growth in cotton textiles to declines in woven and knitted apparel, this article explores the ups and downs of India’s textile export journey over the past one year.

India’s textile and clothing (T&C) sector has experienced a challenging period, witnessing a decline in exports for the second consecutive year. In FY2023-24, T&C exports dropped by 2.33%, totaling US$ 34,836.76 million, down from US$ 35,669 million in FY2022-23. Despite this downturn, the sector’s contribution to the country’s total exports remained steady at 8%.

The top destinations for India’s T&C goods include the USA, Bangladesh, UK and Germany, with the USA remaining the largest market. Among the various commodities, woven apparel and cotton are the leading exports. However, these categories have experienced contrasting trends.

Woven Apparel: A Declining Sector

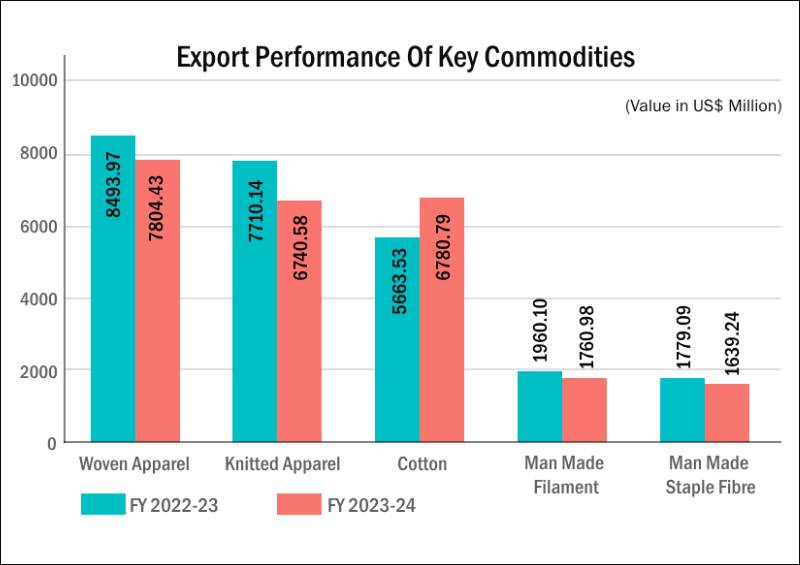

Woven apparel, the largest exported commodity, saw a decline of 8.12% to US$ 7,804.43 million, accounting for 22% of total T&C exports. The most exported item in this segment, women’s or girls’ suits and ensembles, fell by 9.64% to US$ 2,838.01 million.

Men’s shirts, the second most exported item, dropped by 2.46% to US$ 1,056.88 million. Exports to the USA, the largest market for woven apparel, declined by 14.39% to US$ 2,503.86 million.

Knitted Apparel: Witnessing Similar Trend

Knitted apparel, representing 19% of total T&C exports, also declined by 12.58% to US$ 6,740.58 million. The USA remains the largest market, but exports to the country decreased by 10.91% to US$ 2,215.19 million. The largest product in this segment, cotton T-shirts, fell by 12.1% to US$ 1,565.85 million, with an average unit value realization (UVR) of US$ 2.35 per piece.

The Cotton Export Surge

Despite the overall decline in the T&C sector, India’s cotton exports have surged by 19.73%, contributing 19% to the total T&C exports. In FY2023-24, cotton exports amounted to US$ 6,780.79 million. Bangladesh remains the top buyer, importing US$ 2,368.84 million worth of cotton, a 16.76% increase. Notably, China’s cotton imports from India skyrocketed by 275.84% to US$ 924.42 million.

Cotton yarn emerged as the highest exported product within the cotton segment, with exports totaling US$ 3,780.23 million, a growth of 37.34% in FY2023-24 The average UVR for cotton yarn was US$ 3.11 per kg, down from US$ 4.15 per kg in the previous fiscal.

India’s raw cotton exports grew by 42% to US$ 1,128.27 million, with an average UVR of US$ 1.96 per kg. The quantity of raw cotton shipped was 574.30 million kg.

Man-Made Filament (MMF) Faces Decline

Exports of MMF dropped by 10.16% to US$ 1,760.98 million. The most exported product, woven fabric of synthetic filament yarn, declined by 8.88% to US$ 853.52 million. However, the quantity of MMF fabric supplied increased by 7.05% to 1647.25 million sq.m, with an average UVR of US$ 0.52 per sq.m.

Man-Made Staple Fibre (MMSF): Slight Growth in Fabrics

MMSF exports decreased by 7.86% to US$ 1,639.24 million. However, the export of MMSF fabrics saw a marginal growth of 0.67% to US$ 642.46 million, with an average UVR of US$ 1.08 per sq.m. Turkey remains the top export market for both MMF and MMSF, but exports to Turkey declined significantly.

Stable Carpets and Rising Silk Exports

India’s carpet exports remained stable, with a minimal growth of 2.33% to US$ 1,875.55 million. The USA is the largest market, accounting for 58% of this segment’s exports.

Silk exports experienced a notable growth of 22.56%, totaling US$ 124.05 million. UAE and China drove this increase, with exports to UAE growing by 40.49% to US$ 40.74 million, and exports to China rising by 83.67% to US$ 37.50 million.

Country-Wise Trends

China has made a significant comeback, becoming the sixth-largest market for India’s T&C exports with a 152.62% growth to US$ 1,222.16 million in FY2023-24 from fifteenth position in FY 2022-23. Cotton exports to China surged by 275.84% to US$ 924.42 million.

Despite being the largest market, T&C exports to the USA declined by 4.28% to US$ 9,598.97 million. Apparel remains the largest exported commodity, but exports of woven apparel to the USA fell by 14.39%.

Bangladesh is the second-largest market, with T&C exports growing by 11.18% to US$ 2,815.18 million. Cotton exports to Bangladesh grew by 16.76% to US$ 2,368.84 million, making up 84% of total T&C exports to the country.

UAE, the third-largest market, saw a decline of 3.15% to US$ 1,991.96 million. UK, the fourth-largest market, experienced a decline of 6.07% to US$ 1,877.71 million. Apparel exports to both countries declined significantly.

India’s T&C sector faces a challenging landscape with mixed trends across different segments and markets. While cotton and silk exports have shown remarkable growth, woven and knitted apparel, along with MMF and MMSF, have experienced declines. The sector’s future hinges on navigating these complexities and capitalizing on growth opportunities in key markets.