Jute Makers To See Margins Drop For Second Straight Fiscal

Operating margins of jute manufacturers are expected to shrink by approximately 50 basis points (bps) this fiscal due to wage hikes and subdued demand in the more profitable export markets. This marks the second consecutive year of declining profitability.

Despite this, their credit profiles will remain stable due to strong procurement by government agencies, healthy balance sheets and negligible capital expenditure (capex) debt. An analysis of 10 jute companies rated by CRISIL Ratings, which account for around 30% of the sector’s revenue, supports this outlook.

Wages for jute mill workers in West Bengal, which produces almost 80% of India’s jute products, were raised at the end of the last fiscal year following a tripartite agreement between the state government, mill owners and various trade unions. The extent of the wage hikes depends on workers’ experience, with the overall wage bill expected to increase by 5-6% per annum, depending on the level of mill modernisation.

Demand from the US and Europe, which together account for over 60% of exports and a third of the sector’s Rs 12,000 crore revenue, will remain subdued due to the discretionary nature of jute product usage in these markets.

Rahul Guha, Director at CRISIL Ratings, stated, “The impact of wage hikes on operating profitability will be limited due to strong demand from government agencies under the mandatory packaging norms, which account for two-thirds of the sector’s revenue and allow for cost pass-through. However, subdued export demand will weigh on sales of specialised jute products, such as hessian, gift articles and decorative fabrics, which offer better margins. As a result, operating margins of players rated by CRISIL Ratings are expected to fall by approximately 50 bps this fiscal.”

Rahul Guha, Director at CRISIL Ratings, stated, “The impact of wage hikes on operating profitability will be limited due to strong demand from government agencies under the mandatory packaging norms, which account for two-thirds of the sector’s revenue and allow for cost pass-through. However, subdued export demand will weigh on sales of specialised jute products, such as hessian, gift articles and decorative fabrics, which offer better margins. As a result, operating margins of players rated by CRISIL Ratings are expected to fall by approximately 50 bps this fiscal.”

Continued weak export demand will result in low-capacity utilisation of specialised looms, limiting capacity addition. Jute companies will primarily undertake maintenance capex through internal accruals.

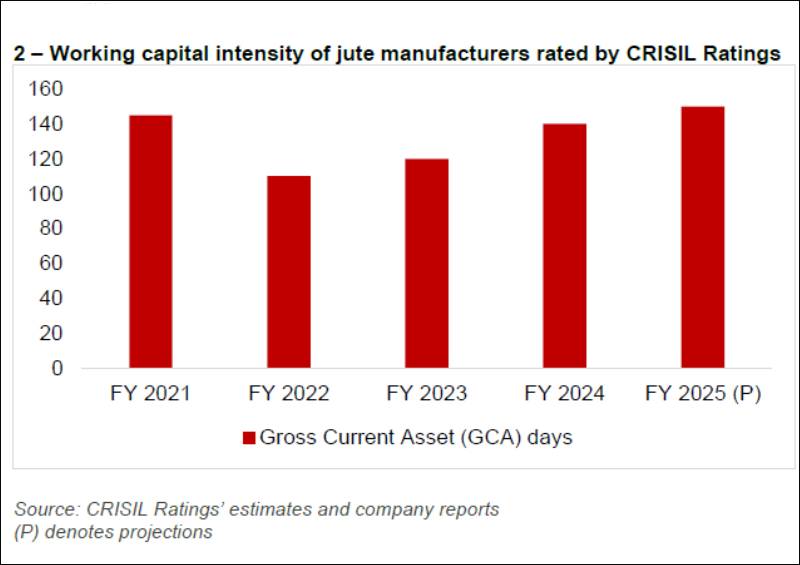

Argha Chanda, Director at CRISIL Ratings, noted, “Minimal capex outlay will lead to limited long-term debt addition for the industry. However, reliance on working capital debt will increase as the working capital cycles of jute manufacturers will be stretched, nearing 150 days, as they continue to provide extended credit to attract overseas buyers. Despite this, the healthy balance sheets of jute manufacturers will keep debt protection metrics comfortable.”

CRISIL Ratings expects the leverage and interest coverage ratio of its portfolio to be at 0.6 times and 3 times, respectively, this fiscal, compared with an average of 0.5 times and 7 times, respectively, over the last three fiscals.

Looking ahead, global recessionary pressures and potential changes in packaging reservation norms for the jute industry will be key factors to monitor.