China’s Cotton Exports Hit 7-Year High Despite U.S. Tariffs

China’s cotton consumption and exports are defying global trade headwinds, even as higher U.S. tariffs and restrictions under the Uyghur Forced Labor Prevention Act (UFLPA) were expected to weigh on shipments. According to the latest World Markets and Trade report from the U.S. Department of Agriculture (USDA), China’s cotton product exports in marketing year (MY) 2024/25 (Aug–July) touched a seven-year high, supported by competitive pricing, robust domestic demand and fiscal stimulus measures.

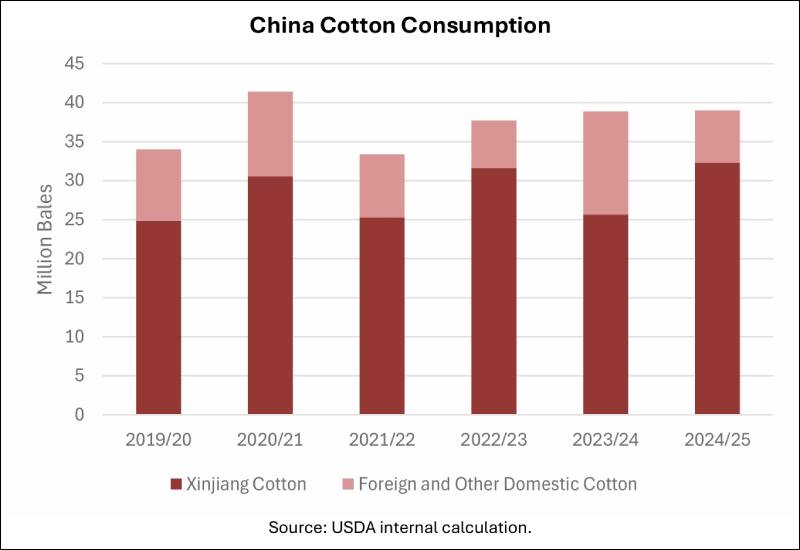

China’s cotton consumption is estimated at 39 million bales in MY 2024/25, unchanged from last year and above earlier forecasts. A record 1.09 trillion yuan in annual domestic apparel sales, backed by government-led demand stimulus, further bolstered mill use. The IMF recently revised China’s GDP growth forecast for 2025 upwards to 4.8%, citing improving consumer demand.

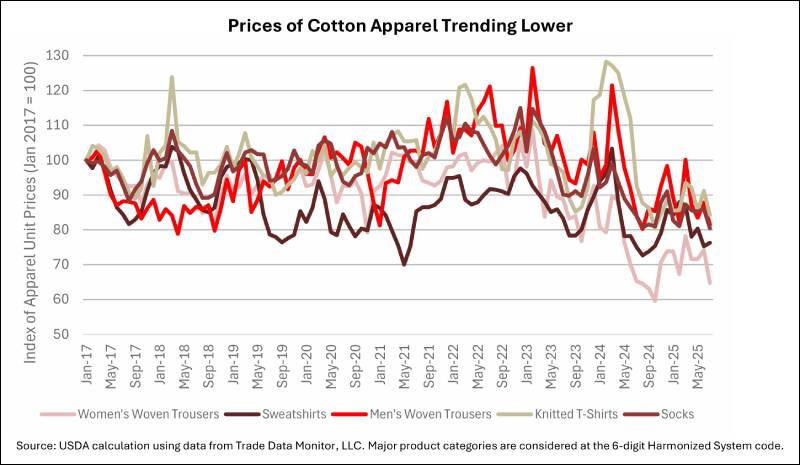

Interestingly, exports to the U.S., China’s largest market for cotton products, surged despite tariff hikes. Frontloading of U.S. imports and lower comparative prices gave China an edge, with July prices for women’s woven trousers, its top category, about 30% lower than eight years ago.

However, the UFLPA continued to impact Xinjiang-origin fibre, forcing China to divert that cotton away from the U.S. market. Imports fell to the lowest in nearly a decade as the government refrained from auctioning reserves, while Xinjiang production reached record highs.

Global Cotton Outlook: Production, Trade and Prices

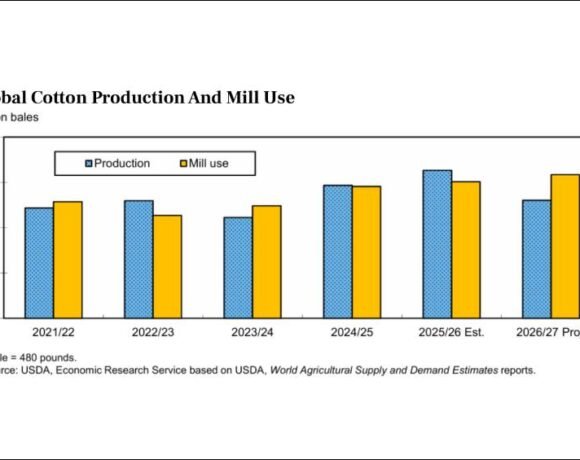

The USDA raised global cotton production for MY 2025/26 by 1.0 million bales to 117.7 million bales, with larger crops in China, India and Australia offsetting declines in Turkey, Mexico and Mali. China alone is expected to produce 32.5 million bales, its biggest crop in 12 years.

Global trade is forecast at 43.7 million bales, marginally higher than last month’s estimate. India and Australia are expected to raise exports by 300,000 bales and 100,000 bales, respectively, while Cameroon, Côte d’Ivoire and Mali will see lower shipments. On the import side, Vietnam, Turkey and Mexico are projected to buy more, offsetting reduced demand from India and China.

Consumption is projected at 118.8 million bales, led by a 1.0-million-bale increase in China, even as Turkey’s use moderates. Global ending stocks are now forecast at 73.1 million bales, nearly 800,000 bales lower, driven by stronger consumption.

Price Trends

Cotton futures on the Intercontinental Exchange (ICE) held steady at 66 cents per pound, while the global benchmark A-Index was quoted at 77.9 cents per pound in September, nearly unchanged from August. Country-wise, spot prices diverged — rising in China to 97.4 cents/lb, while easing sharply in India, Brazil and Pakistan.

The USDA retained its forecast for the U.S. season-average farm price at 64 cents/lb for MY 2025/26.

India: Higher Output, Stronger Exports

India’s cotton production for MY 2025/26 has been revised upwards to 24 million bales, with exports projected at 1.3 million bales, a 30% jump from the earlier estimate. This follows improved crop conditions, though domestic use is steady at 25 million bales. Imports are forecast slightly lower at 2.8 million bales due to better local availability.

The Bottom Line

The cotton market is entering MY 2025/26 on a stronger footing, with China driving both consumption and exports despite geopolitical headwinds. Record Xinjiang output, resilient domestic demand and competitive pricing are supporting trade flows, while higher global production from major growers like China, India and Australia is expected to keep supplies ample.

With futures and spot prices relatively stable, the market’s trajectory will now hinge on the pace of global demand recovery, evolving U.S.-China trade relations, and weather developments across key growing regions.