Global Cotton Market Tightens As Production Falls And Demand Rises In 2026-27

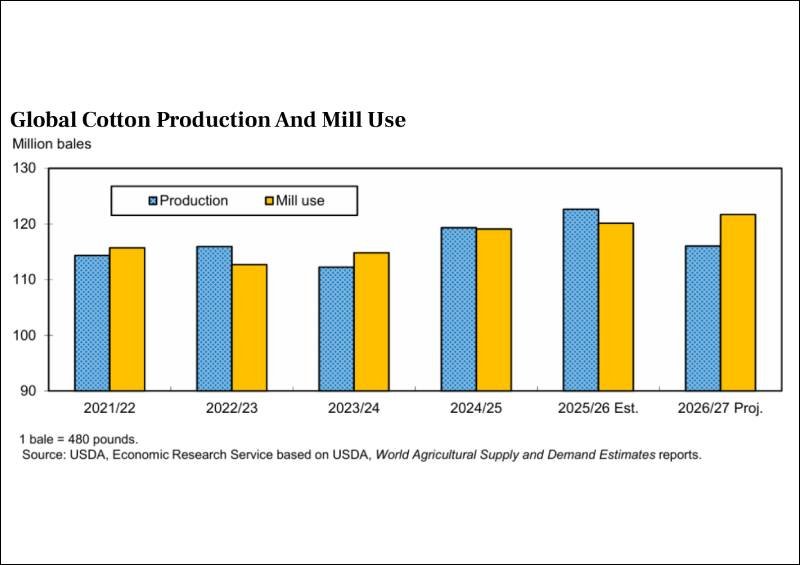

The global cotton industry is heading into a tighter supply cycle for the 2026-27 season, with lower production forecasts and steady improvement in mill consumption expected to reshape pricing dynamics across major cotton producing and consuming regions. According to the latest Cotton and Wool Outlook: May 2026 released by the U.S. Department of Agriculture (USDA), world cotton ending stocks are projected to decline significantly as mill use is expected to outpace production for the first time in three years.

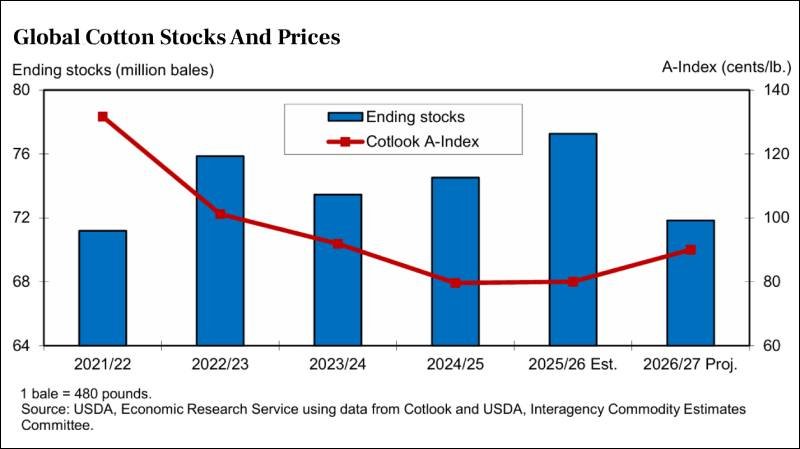

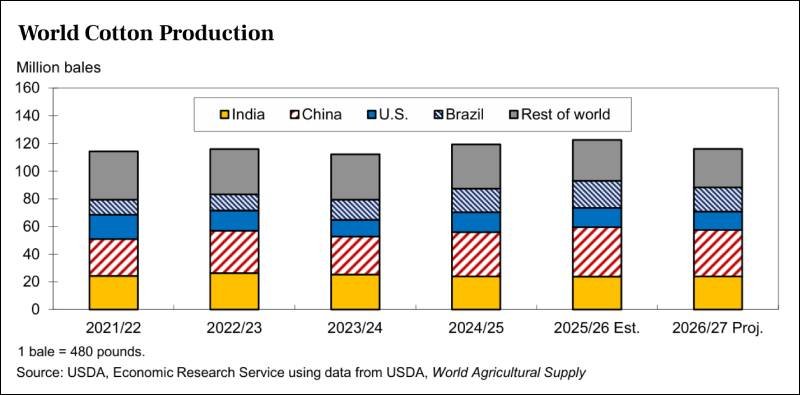

USDA estimates global cotton ending stocks for 2026-27 at 71.8 million bales, a decline of 7 per cent compared with the previous season. The reduction is largely driven by a projected fall in world cotton production, which is expected to decline by 5 per cent to 116 million bales, while mill consumption is forecast to rise modestly to 121.7 million bales. This imbalance is expected to provide upward support to cotton prices, with the global A-Index projected to rise to 90 cents per pound, up from 80 cents in 2025-26.

Production Declines Across Key Growing Nations

The report projects lower production across most major cotton-producing countries, with the notable exception of India.

China, the world’s largest producer, is expected to see output fall to 33.5 million bales, reflecting lower yields following two consecutive years of exceptional crop performance. Brazil is also forecast to register its first production decline in five years, with output expected to fall by 2 million bales, while Australia’s production is projected to plunge 33 per cent due to reduced water availability. The United States is expected to produce 13.3 million bales, lower than the previous season.

India, however, stands out as the only major producer expected to post a marginal increase, with production forecast at 24 million bales, supported by higher harvested area despite slightly lower yields.

Weather Concerns Cloud U.S. Outlook

The U.S. cotton sector faces mounting weather-related challenges, particularly in the Southwest.

USDA notes that nearly 98 per cent of U.S. cotton production area is currently affected by drought conditions, a sharp contrast to just 20 per cent a year earlier. While planted area is estimated to increase to 9.64 million acres, harvested area is expected to decline because of higher abandonment rates, especially in Texas, where moisture deficits remain a serious concern.

Despite these challenges, U.S. cotton exports are projected to rise to 12.3 million bales, marking the highest level in four years. Ending stocks are forecast to fall to 3.9 million bales, with the average upland farm price projected at 73 cents per pound, significantly above the previous season’s estimate of 63 cents.

Mill Use Continues Recovery

Global cotton consumption is expected to continue its recovery trajectory for the fourth consecutive year.

The report attributes this growth to improving global GDP prospects, replenishment of textile and apparel inventories, and stronger consumer demand for clothing. China and India will continue to dominate global cotton consumption, together accounting for more than 55 per cent of world mill use. China’s mill consumption is forecast at 41 million bales, while India is expected to reach 26 million bales, matching its previous record.

Other major spinning nations such as Pakistan, Bangladesh and Vietnam are also expected to post moderate growth, reinforcing Asia’s central role in the global cotton value chain.

Trade Flows Shift Toward Asia

Vietnam is forecast to become the world’s largest cotton importer in 2026-27, with imports reaching a record 8 million bales, followed closely by Bangladesh and China. These three countries are expected to account for nearly 53 per cent of global cotton imports, reflecting continued investment in textile manufacturing and export competitiveness across Asia.

Meanwhile, Brazil and the United States are expected to strengthen their dominance in cotton exports, together accounting for nearly 63 per cent of global trade.

A Firmer Price Outlook Ahead

With global stocks projected to fall to their lowest level since 2021-22 and the stocks-to-use ratio reaching a six-year low, the cotton market appears poised for firmer pricing in the coming season.

For textile manufacturers, spinning mills and sourcing strategists, the evolving balance between supply constraints and resilient demand will be critical to monitor. As weather uncertainties persist and production risks remain elevated, the 2026-27 season may mark a turning point for global cotton markets, one that could reshape procurement strategies and pricing expectations across the textile value chain.